What is the difference between providing good HELOC and you will refinancing my mortgage?

When you could potentially be eligible for a borrowing limit away from right up so you can 65% of your own home's value, your own real maximum is susceptible to an inconvenience test similar with the home loan stress test. Financial institutions or other federally controlled lenders use the greater regarding either:

- the lending company out-of Canada four-seasons standard rates, currently set-to 5.twenty-five %, and you can

- the discussed rate of interest together with 2%.

to choose their borrowing limit. It's also possible to feel subject to then limitations centered on the credit history, proof earnings, and you may latest debt account together with mastercard and you may car loan financial obligation.

Refinancing your own mortgage enables you to obtain a swelling-sum in the home financing rate of interest which is constantly lower than what you would be capable of geting with the an effective HELOC. In place of a HELOC, not, you're going to have to create normal repayments torwards your own mortgage that is each other prominent and you can mortgage payments. Having a good HELOC, you possibly can make appeal-simply repayments, somewhat reducing the amount you only pay back each month. That is useful if you will simply be in a position to make a cost sometime later, like in the actual situation away from remodeling your house.

To have a HELOC, the interest rate is generally a creditors perfect rate + 0.5%. Finest Prices are ready of the loan providers and certainly will vary from business so you can insitution. It indicates, in place of the fresh new fixed money inside the a predetermined-price mortgage, good HELOC's rates is actually varying. So if a lender grows their perfect rates, in that case your HELOC desire payment expands. The fresh new cost is actually typcially greater than the rate of the initial home loan.

Mortgages in addition to often incorporate pre-commission limits and you may penalties. You will not have the ability to pay extent your lent quickly, and it will continue to accrue attract. A beneficial HELOC, on the other hand, offers the flexibleness so you're able to obtain and you can pay-off the credit whenever you want.

What is loans Park Center the difference in providing a great HELOC an additional mortgage?

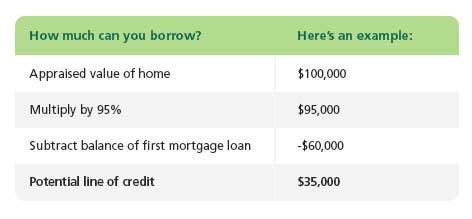

When you're both a HELOC and a second mortgage use your house collateral as collateral, a second financial could offer your the means to access a high total credit limit during the increased interest. This really is around 95% of the house's value as compared to 65% restriction getting good HELOC. The difference between your HELOC because a line of credit and you may the second home loan given that that loan nonetheless implement: which have a good HELOC, you reach obtain and you will repay in your agenda if you're you could simply acquire a fixed lump-contribution of a second home loan and just have to make payments for the next home loan toward a predetermined plan.

The lender to suit your 2nd mortgage is not usually the same since your first lender the person you do usually get the HELOC away from. You will have to check around to find the best conditions.

Are a great HELOC much better than a home loan?

This will depend. If you have look at the a lot more than parts, then the answer alter a variety of things. Ponder concerns instance, just how much ought i finance? Exactly why do I would like the bucks? Would You will find an excellent economic abuse getting an effective HELOC? Just how much security might have been built-into my personal house? Just after reflecting towards the questions such as, the solution to your financial needs is to end up being obvious.

Most other factors whenever making an application for good HELOC

Obtaining a beneficial HELOC may potentially affect your credit score . They will act as a great rotating line of credit, the same as a charge card, and a premier application price can also be negatively perception your credit score. In the event the made use of accurately , yet not, it does decrease your complete credit usage rates and you may try to be a confident sign of good credit actions.